BBF305/03: Evaluate the three mutual funds using Sharpe and Treynor measure and Given the risk-free rate is 5%: Investment and Portfolio Management Assignment, WOU, Malaysia

Assignment Type

Individual Assignment

Subject

BBF305/03: Investment and Portfolio Management

Uploaded by Malaysia Assignment Help

Date

06/28/2022

QUESTION 3

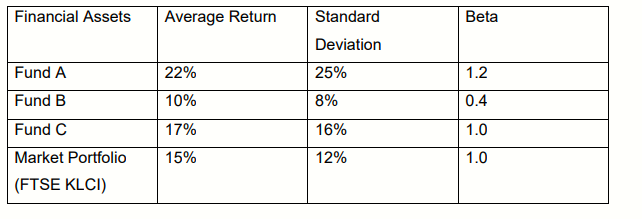

Evaluate the three mutual funds using Sharpe and Treynor measure. Given the risk-free rate is 5%.

a) Calculate the following measures for each fund and market portfolio:

i) Sharpe measure

ii) Treynor measure

b) Rank the portfolios using both measures and discuss the differences you find in the ranking.

QUESTION 4

a) You are in a senior management position in a leading international funds management firm. Your Board of Directors required you to analyze FOUR (4) benefits of allocating funds across various countries and geographical regions based on two market dimensions:

i) Developed countries.

ii) Emerging markets.

Get 30% Discount on This Assignment Answer Today!

Get Help By Expert

do you need BBF305/03: Investment and Portfolio Management assignment help? then assignment helper Malaysia is ready to take care of your assignment and offer authentic and reliable solutions for accounting assignments and management assignments at a reasonable price.

Recommended Assignments for You

Related University Assignments

- MPU3183 Appreciation of Ethics and Civilisations Assignment Brief 2026

- TEE314 Microelectronics Course Assignment 2 Brief 2026 | WOU

- MPU3193 /MCMPU3193 Philosophy and Current Issues Assignment 2, 2026

- MCBMG311/03 Micro – Credential in Employment Law and Industrial Relations Assessment 3 Question 2026 | WOU

- TEE208/03 Circuit Theory II Assignment 2, 2026 | Wawasan Open University

- TEL 203/03 Process Control and Instrumentation Course Assessment 2 (CA2 – 30%)

- The Challenges Teaching English to Refugee Children Research Proposal Case Study

- TEE106/03 Basic Electromagnetic Theory Assignment 1 (25%)

- WUC118/03 Computing & Digital Transformation Assignment: Case-Based Analysis on Cloud, Cybersecurity & Emerging Technologies

- BMG 323/03 (BBM023/03) Clustering and Predictive Analysis Assignment 2: Homestay Case Study for Data-Driven Business Optimization in Malaysia

Convincing Features